Vietnam’s market has had some challenging years recently. When global spending began to normalize from late 2022 / early 2023 after a period of strong recovery post-COVID, retailers in Vietnam’s key export markets such as US and EU, seeing their inventories piling up, put a hard pause on buying. Vietnam’s exports slumped as a result. And while foreign tourists hadn’t really come back post-COVID, the economy that is mainly backed by exports and tourisms, and which, prior to COVID, had been growing at 6-7% p.a., came to a halt. Coupled with the bust of property bubble, domestic consumption literally evaporated overnight. But just like in every economic cycle, if you can still believe in a sustained long-term tailwinds for the Vietnamese economy, it was a golden opportunity to increase exposure to Vietnam equities.

From a year ago until today 5 Jul 24, my portfolio of very concentrated bets in Vietnamese companies has returned >32%. It could have been much better had I stepped on the gas early on instead of buying in gradually over months in an overly conservative manner. The lesson here is that when you see a clearly compelling opportunity with strong conviction, you bet aggressive! This was not the only mistake I have made for the past year (It is the topic for another day). This return, however, says nothing about tomorrow, or a year from now, or the future longer term. After all, the compounding journey is not a sprint but a marathon. My goal is to 10x after 10 years and 100x after 20 years.

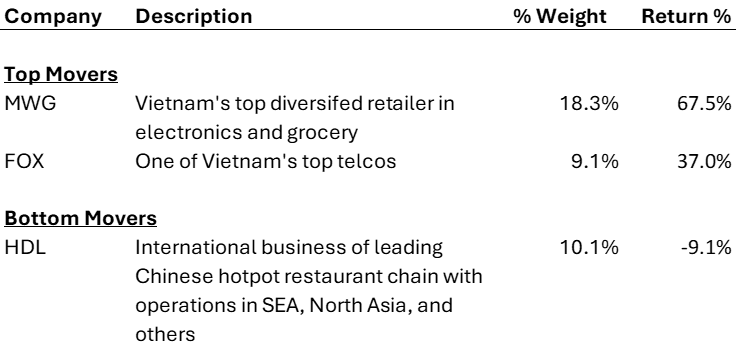

Some highlights in my current equity portfolio:

The current bottom mover is a business that I admire. They are not a Vietnamese company but have substantial business in Vietnam that I can understand. I will write about my thesis here when my schedule allows.

Unlike other fund managers who would have 20-30 stocks in their portfolio, the top 5 holdings account for ~70% of my portfolio and the overall portfolio has no more than 10 companies. The top 5 companies are what I consider my “coffee can” portfolio, whose business I can understand and which I believe are long-term compounders with long growth runway still ahead of them. What you’d want to do with these wonderful businesses is just to put them in a coffee can and keep under the bed for a very very… long time.

The rest of my portfolio is more opportunistic – good value opportunities, decent businesses available at cheap price, but unlikely to be long-term compounders. To be honest, I still find it hard to ignore such opportunities, where I believe there’s temporary mispricing by the market that should correct soon. As mentioned previously, the downside of investing in these just-good-enough businesses at cheap price is that you would have to keep finding them and recycling your capital. Yes, I still have FOMO, which I will rectify over time.

Risk

A primary reason why the Modern Portfolio Theory says you should own a portfolio of ~30 stocks to optimize risk-adjusted returns is that it considers risk as the volatility in stock price (beta) and the extent to which different stocks in the portfolio move in tandem (correlation). As such, by owning as many as 30 stocks in the portfolio, you can reduce the chance of all holdings in your portfolio go down in flame at once, while still maintaining the upside returns.

If you think like a business owner who would focus on business fundamentals or earnings instead of stock price, you obviously would no longer care about “beta” and “correlation”. When you buy a stock, instead of thinking of it as a number on the screen, think of it as your partial ownership in a business. Warren Buffet says to only invest in businesses that you would be comfortable holding even when the stock exchange is closed down tomorrow. This is where there is no difference between public market and private market investing. Risk is not “beta”, risk is the chance that “your” business deteriorates or loses its competitiveness over time, leading to permanent loss of capital. Or in another case, the business still performs, but you overpay for the asset, leading to low returns on investment.

Very often I hear people expressing their concerns over price volatility or liquidity of a stock. I just think it’s hysterical. If you invest to enjoy the profits generated by the business, why should price volatility or liquidity of the stock matter? Those are only risks when you allow them to be. And that is by having a short-term horizon and using excessive leverage.

I would, in fact, prefer a stock with high volatility – great, Mr. Market seems very emotional about the company and never makes up his mind about the value of the business. And when I see a stock with low liquidity – awesome, no one has noticed about this company yet.

Vietnam

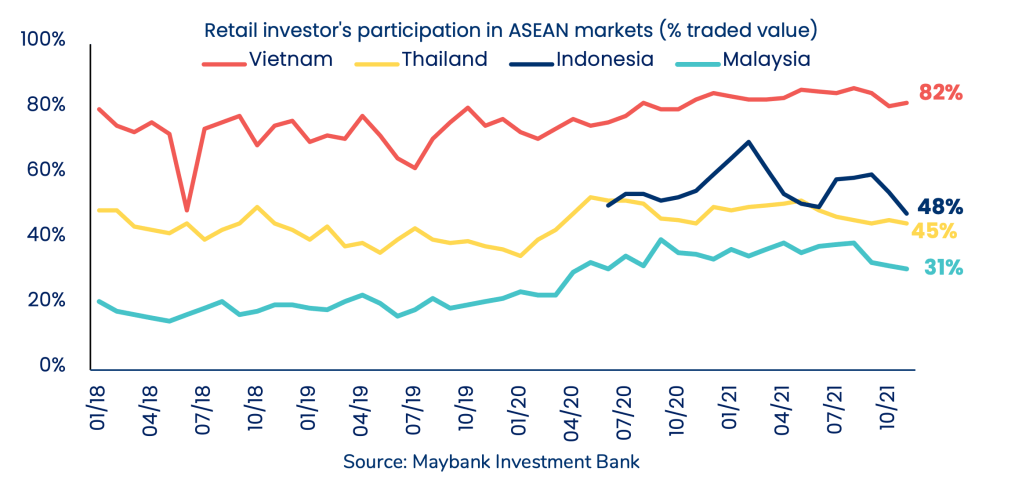

When talking about the Vietnamese market, I would not bore you with the usual narrative you must have heard a thousand times from everybody and their mothers – fast-growing economy, rising middle-class, growing foreign direct investments, expanding trade and production, increasing digital penetration, pro-trade government, etc. After all, that is the common theme across most countries in Southeast Asia. There is one thing unique about Vietnam’s equity market, though, which makes me particularly interested in. And that is the very high participation of retail investors in the equity market compared to other peers in the region.

I was fascinated by this chart – if this is true, it means Mr. Market in Vietnam is crazier and way more emotional and irrational than other markets in SEA!

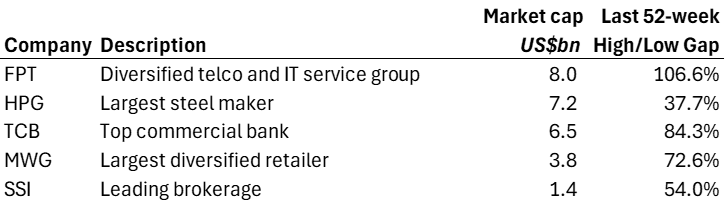

Looking at companies in the VN30 index – Top 30 Vietnamese stocks with the highest market cap and liquidity, you can always see a big gap between their 50-week highs and lows over time. For instance:

These are only five companies I picked randomly, when you expand the period (beyond the last 52 weeks) and move down the list by market cap, you will see the High-Low gap widen even further. No doubt Vietnam is still a young economy and things can get choppy sometimes. But for billion-dollar businesses like these, there is absolutely no reason their value should vary by 80-100% in the span of a year. This is where I believe it presents huge opportunities for smart and patient capital. Why taking risks by investing in private businesses or venture capital with high uncertainties plus zero governance nor transparency when you can achieve this kind of returns in public companies, which by the way are still growing like weed at attractive ROIC (again, thanks to Vietnam’s economic tailwinds), is what I was thinking to myself when I saw these data.

When you talk to most people about investing in Vietnam’s public equities, they would say it is extremely risky because of the stock price volatility. As mentioned above, those people think of risk as “beta”, they invest for non-investment reasons. I genuinely believe in a market such as this, to get rich, you do not have to be a business genius, just have to be patient and rational when others are not. But of course, the latter seems no easier than the former.

Currently, there is a golden opportunity to buy into Vietnam. Coupled with heightened economic uncertainties (both domestically and in key global export markets), US’ elevated interest rates have driven short-term capital away from developing markets like Vietnam back to the US, strengthening the US dollar. This has resulted in a massive outflow of capital in major foreign ETFs that have Vietnam exposure, causing these funds to sell Vietnam equities blindly at any price. You may think these “institutional” investors are smart capital, but really that is literally dumb money.

When people ask me whether I am concerned about the massive outflow of foreign capital from Vietnam’s equities (which started since 2023), I would just tell them to instead look at the inflow of foreign direct investments in setting up production and businesses in Vietnam, which has risen every single year, without fail, for the past decade (barring the two flat years during COVID). To put things into perspective, while foreign investors have so far “withdrawn” >$2bn from the Vietnam’s equity market in the last 12 months, foreign direct investments (FDI) from global companies into Vietnam continue to top >$20bn in the same period. The former is speculative money, the latter is long-term fundamental. As a patriot, I’d like to say this is when local Vietnamese get to buy back our good assets from the foreigners.

This window of opportunity, however, could be closing very soon. The government has made it their top priority to upgrade Vietnam’s stock market from frontier to emerging market status. Once that happens, more foreigners with their stronger currencies will flock in and scoop up high quality assets. That is when you would see the pool of opportunities become much more limited.

So there, without telling you what you have already known, why I think Vietnam NOW is a good idea.

****

I have been given some suggestions on what to discuss here, which I will try to write about over time. I appreciate all of your feedback thus far.

If you’d like to talk investment ideas and welcome others’ thoughts without being overly defensive, please do reach out. I am always interested in meeting like-minded folks to exchange investment ideas, AND book recommendations as well.

For those who are new to this site, for instant updates, the Subscribe button is at my home page. You will then have to go and click confirm in your email. It is completely FREE!

Leave a reply to Hannah Cancel reply